Don’t Toss That Mail!

We all get so much mail – both the paper stuff and the kind that comes electronically – it’s understandable that we sometimes toss things that don’t look pertinent.

But wait! Before you hit the delete button or head to the shredder with that Plan and Investment Notice you got from TIAA-CREF this month, take a moment to review it. After all, those fees come out of your retirement savings. Don’t you want to know how much you’re paying and if you can do better?

About Fees

All investment funds charge fees. Fees cover the cost of the administration of the fund. There’s no free lunch, and there’s no free investing.

Generally speaking, fees vary depending on how much work is involved in managing the fund. That’s why a fund that is indexed to something like the S&P 500 will have a lower fee than one that is more actively managed. The index fund’s stock composition is based on a pre-existing list of securities, so it’s less expensive to administer than a fund where investment professionals are trading stocks in and out of the fund on a regular basis.

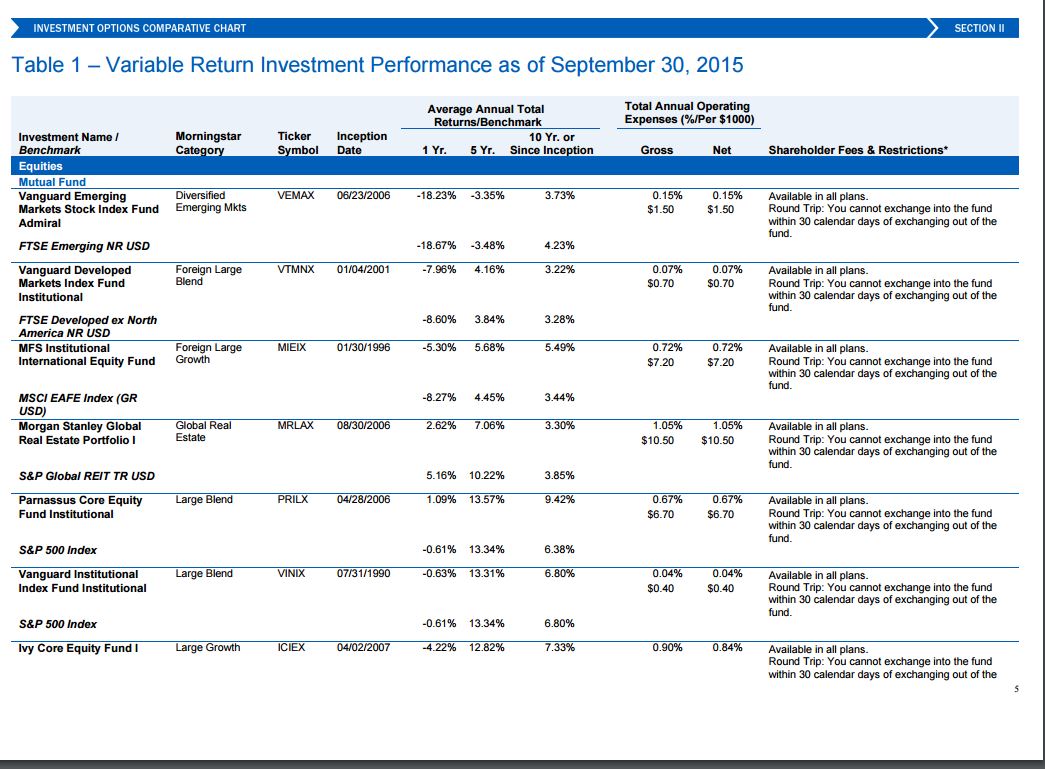

The Expense Ratio is the fee charged to operate and manage an investment expressed as a percentage of the investment’s assets. For example, an expense ratio of 1.5% means that each year, 1.5% of the investment’s total assets are used to cover the fund’s expenses. This number gives you an “apples to apples” way of comparing the fees of various investments.

You can find the Expense Ratio for each investment option in the “Total Annual Operating Expenses” column of the Investment Options Comparative Chart you will receive in your Fee Disclosure. You can learn more about Expense Ratios and review an example of how they can affect your plan accumulation over time on the TIAA-CREF website.

About The Fee Disclosure

The goal of the Fee Disclosure is to give you the information you need to make decisions about your own retirement investments. The report (sample page below) shows you the fees assessed for each of the funds you can invest in via the Lehigh University Retirement Plan. It also shows you the past performance of those funds. Past performance is not a guarantee of future performance; however, it does give you additional data to consider.

What To Do With What You Learn

Now that you’ve rescued your Fee Disclosure from the trash and combed through it, what should you do with your new-found knowledge?

For many of us, the answer is to do nothing. If you feel that your investment savings are allocated to a good mix of funds and are comfortable with the fees, then you’re all set.

If, however, you think you need to make a change, simply go to the Lehigh University Retirement Plan microsite and re-balance your allocations. While you’re there, remember to increase your voluntary contribution to 6 percent so that you will maximize your match starting January 1, 2017.

Keep In Mind

Fees are important but they are just one aspect to consider when you’re making decisions about where to invest. They can and do impact the overall amount of money you have in your retirement savings. However, more important to the success of your retirement savings planning are the amount you are putting aside, and the allocation of that money into various funds that have different levels of risk and return.

If all of this sends you to the medicine cabinet for aspirin, why not get some solid, free advice from the financial consultants of TIAA-CREF? A trained counselor is on campus twice monthly, and you can make an appointment to sit down with her or him by calling TIAA-CREF directly at 1-800-732-8353.